Navigating the Market: Expert Insights and Positive Trends

In the days following the election results, there has been a flurry of activity and updates regarding the economy and its influence on the housing market. While the Fed cut rates a quarter point last week, this move did not directly impact mortgage rates, which have continued to tick upwards, with 30-year mortgage rates ranging from the mid-6s and up, depending on several factors. Economists, Lenders, Real Estate Professionals, and potential homebuyers alike continue to watch these numbers closely, with new data and outlooks being published almost daily.

Despite recent moderate swings in interest rates and the activity in the financial markets, many analysts anticipate mortgage rates to stabilize in the upcoming weeks and months at a rate below this year’s levels.

The National Association of Realtors (NAR) Chief Economist, Lawrence Yun, gives his take on the real estate market, noting, “Housing affordability has been a challenge, but the worst appears to be over. Rising wages are outpacing home price increases. And more inventory is reaching the market, providing additional options for consumers.” For homebuyers, this is certainly welcome news.

NAR reported housing affordability actually improved slightly, which is good news for many. Monthly mortgage payments are down 5.5% from the second quarter of 2024 and down 2.4% from one year ago.

With much talk about interest rates and predictions about the future economy, Yun gives encouraging updates for homeowners, referencing national data stating that on average, a typical homeowner accumulated upwards of $147,000 in housing wealth in the last five years. He notes that home prices remain on solid ground, reflected by the vast number of markets experiencing substantial gains. “Even with the rapid price appreciation over the last few years, the likelihood of a market crash is minimal,” he says. “Distressed property sales and the number of people defaulting on mortgage payments are both at historic lows.”

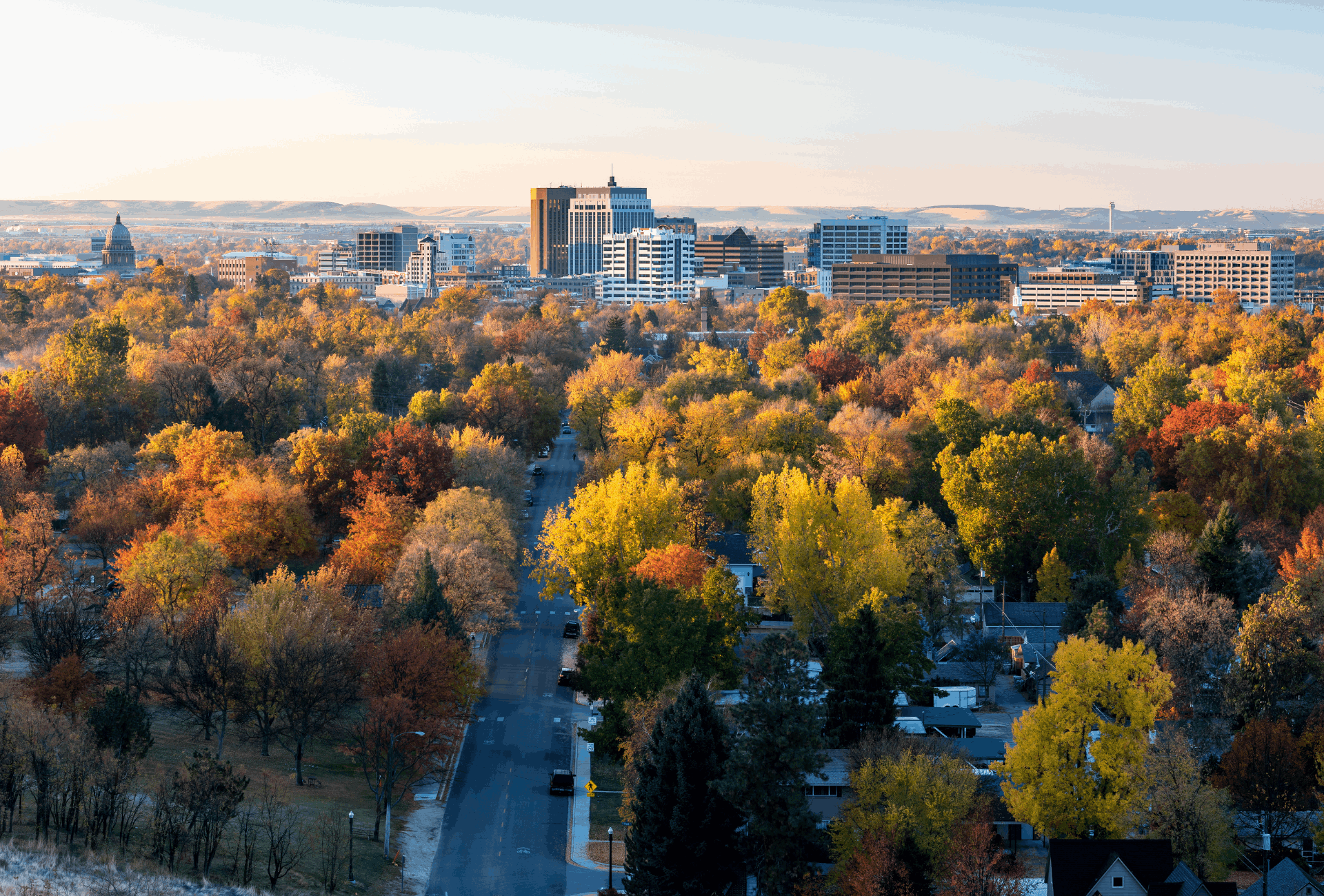

As presented in an article recently published by the Idaho Business Review, median prices on single-family homes throughout the US have continued to steadily climb. The vast majority of Idaho’s counties reflecting a similar trend - In Twin Falls County, the median single-family home price was up 6.8% to $449,000; Bonneville County was up 4.7% to $450,000; Ada County was up 3.3% to $608,425; and Bannock County was up 0.1% to $399,900.

Categories

- All Blogs (284)

- 30thanniversary (1)

- activities (158)

- agents (17)

- announcement (1)

- apartment (1)

- april (2)

- architecture (3)

- art (7)

- art festival (2)

- article (1)

- august (3)

- awards (3)

- beer (4)

- biking (1)

- boise (145)

- Boiseevents (126)

- boisehousing (12)

- boiseriver (13)

- brew festival (6)

- buyers (35)

- campgrounds (1)

- camping (2)

- cars (1)

- children (22)

- christmas (4)

- cincodemayo (1)

- coffee (1)

- communities (3)

- concert (8)

- condominium (1)

- couples (3)

- development (4)

- downtownboise (60)

- downtownyproject (1)

- eagle (9)

- east boise (1)

- easter (1)

- event (11)

- fair (7)

- fall (15)

- family (1)

- familyfriendly (63)

- farmersmarket (13)

- Father's Day (2)

- fathersday (1)

- fest (5)

- festival (6)

- food (5)

- funfacts (2)

- galentines (1)

- garden (5)

- halloween (1)

- holiday (14)

- holidays (23)

- homechecklist (19)

- homeowner (2)

- hotsprings (2)

- housing (20)

- idaho (37)

- idaholife (100)

- idaholifestyle (107)

- july4th (4)

- kids (22)

- laborday (1)

- landmarks (1)

- lifestyle (88)

- listings (16)

- livelocal (49)

- Mandy (1)

- market (7)

- markettrend (1)

- marketupdate (12)

- may (2)

- memorial day (1)

- meridian (1)

- mortgage (3)

- mothersday (2)

- mountain (1)

- movies (2)

- museum (3)

- music (3)

- music festival (10)

- musical (1)

- nampa (3)

- NAR Settlement (1)

- neighborhoods (32)

- news (1)

- outdoorrecreation (88)

- outdoors (90)

- parks (44)

- pool (1)

- property taxes (1)

- ranking (1)

- realestate (48)

- realestatemarket (29)

- recreation (98)

- restaurants (27)

- run (1)

- sellers (35)

- september (3)

- shoplocal (25)

- shops (36)

- spring (6)

- st patrick's day (1)

- summer (15)

- team (2)

- thanksgiving day (3)

- thingstodo (157)

- tips (100)

- trails (1)

- treasure valley (9)

- trends (7)

- valentines (2)

- waterpark (1)

- wine (5)

- winery (9)

- winter (17)

Recent Posts

Best Neighborhoods to See Christmas Lights

5 Events in Boise & Beyond - December 13th - 15th

Driving in Idaho's Winter Conditions

Young Families Leaving Large Cities For Smaller Towns

5 Events in Boise & Beyond - December 6th - 8th

The Art of Selling a Home During the Holiday Season

What You Need to Know About Cutting Your Own Christmas Tree in the Treasure Valley

Guide to Shopping Local This Holiday Season in Boise

5 Events in Boise & Beyond - November 29th - December 1st

The Lysi Bishop Team Receives #1 Ranking